Picture this scenario: You’re 10 minutes late for work. You do a quick stop at the AXS machine, hoping to pay off your bills before sneaking quietly into the office. There’s like one old dude in front of you. 5 minutes pass. He’s taking forever. He probably doesn’t know how to use the machine. You kinda want to help him out, but you’re already late for work, so you decide to rush to the office first, reminding yourself to pay your bill later.

Picture this scenario: You’re 10 minutes late for work. You do a quick stop at the AXS machine, hoping to pay off your bills before sneaking quietly into the office. There’s like one old dude in front of you. 5 minutes pass. He’s taking forever. He probably doesn’t know how to use the machine. You kinda want to help him out, but you’re already late for work, so you decide to rush to the office first, reminding yourself to pay your bill later.

Your boss yells at you for being late. Your workday gets really busy, and you spend all day fighting fires and solving other people’s problems. Your credit card bill lies forgotten at the bottom of your briefcase. You only remember it three days later, when your credit card company tells you that they’re slapping you with a late-payment charge because you didn’t pay off your bill on time. You start contemplating if you should renounce all your material possessions, move to Tibet, and become a monk.

We’ve all been there. But read on before you start shaving your head – I think you might find this useful.

How I Save Hundreds of Hours on My Finances

Here’s the one crappy thing about personal finance: It takes up so much friggin’ time.

No, really. Think about it. If you’re like most people, you probably do at least some of the following activities every month:

- Queuing up at ATMs, AXS machines, and EZ-Link machines

- Queuing up at banks

- Arguing with some grumpy bank teller

- Negotiating with a customer service rep to waive your credit card fees

- Figuring out how much you spent

- Checking your credit card bill

- Figuring out what you should do with your savings

- Deciding what to invest in

- Transferring money between your own accounts

- Monitoring your portfolio

I’ve tested this out: Administrative tasks like these can easily take up to three to four hours of your time every single month.

Isn’t that crazy? Most people don’t even realize that they’re letting thousands of hours slip away over their lifetimes. That’s three hours a month spent stuck in a queue waiting to give money to some dumb machine. That’s three hours gone forever from your life, which you could have spent having drinks with your friends or watching World War Z (saw it yesterday and totally loved it btw).

Well, screw that.

I now spend no longer than one hour every month on my personal finances, and that’s only because I’m a total weirdo who tracks his spending, portfolio and net worth to the dollar. If you’re not as OCD as I am, it’s entirely possible to get all your administrative tasks done within just a couple of minutes every month.

How do I do it? Simple: I outsource my finances to my personal army of robots. I tell them what to do, and they execute it for me. All I have to do is sit back and make sure that everything’s running as smoothly as a well-oiled machine.

In other words, I automated my finances, and it has made my life infinitely easier.

Why Most People are Afraid of Automation

Most people tend to get really nervous whenever I talk to them about automating their finances. They’ll say things like

“The only way that I can watch my spending is to pay my bills myself.”

“I’m afraid of fraudulent payments”

“I actually really love counting my receipts”

Like I’ve argued before, it’s way easier to come up with reasons on why we don’t want to change our habits, rather than truly test our assumptions out:

Excuse #1: “The only way that I can watch my spending is to pay my bills myself”

Most people assume that once they automate their finances, they’ll end up not caring about how to manage their money, or anything else in life. They’re really afraid that they’ll turn into one of those fat lazy humans on the mothership in Wall-E.

Wrong. When you automate your finances, it actually becomes easier to track your spending. In fact, you’ll know exactly where your money is going to every month, whether it’s in spending, saving or investing.

The only difference is, once you tell your money where it should go, your personal robot army will take over and execute all the boring, mundane things that you don’t want to do, like queuing up at AXS machines.

Excuse #2: “I’m afraid of fraudulent payments”

Okay, it’s perfectly legit to be concerned about fraud. After all, you don’t want some fat 45 year-old lady in Florida to be charging all her massage sessions to your credit card.

Still, automating your finances doesn’t mean that you simply stop checking your bills and statements. You still have to do your own checks, but they won’t take more than just a couple of minutes every month once you create an SOP for doing so. In fact, it’s entirely possible to build a system to ensure that you don’t overlook any of your checks.

Excuse #3: “I actually really love spending 5 hours a month counting my receipts”

You’re really weird. Maybe you should be an accountant.

Why Automate? Three Big Picture Reasons

Here’s the thing: Automating your finances doesn’t just make your life easier – It benefits you in a couple of other important ways:

It keeps your focus on the important things

When I first started my new job, one of my roles was to generate dozens of reports every week. (I know right, super exciting stuff). I earnestly spent hours and hours every day checking through numbers, cross-checking them against other reports, and tweaking Excel formulae.

In short, I focused intensely on the minutiae, and not enough on the big, strategic stuff. I could describe the intricacies of a certain Excel formula, but I couldn’t tell you how our sales were doing, or which markets we should be focusing on, which was my primary job.

I soon lost touch with what my bosses wanted, my performance deteriorated, and I was miserable for most of the day. After realizing that, I refocused. I spent several weeks creating systems of automatic checks, and trained several people to run a few reports on their own. With these micro issues sorted out, I could then focus my energies on making real improvements to my company’s performance instead.

I learnt a valuable lesson from that experience: that everyone has a finite amount of focus, like the amount of physical strength or endurance in your body. Psychologists refer to this as limited cognition.

Mundane tasks like topping up your EZ-Link card or paying off your bills do more than just waste a couple of minutes of your time – They also deplete your focus and take up valuable real estate in your head. Automating them frees up your mind to focus on the more important, game-changing areas in your life, like investing in your personal capital.

It guarantees success

When I was a kid, I used to love getting ang paos for Chinese New Year. I would dream of splurging all of it on things like McDonald’s Hello Kitty dolls GI Joe action figures and Happy Meals.

Fortunately, my parents refused to let me keep any of the money I collected. I wailed like a bratty little kid, but my parents would take that money and deposit it right into a savings account. And 25 years later, I’m super glad that they did that or I might have starved to death in college.

Deep down inside, we’re all still little kids with our own stashes of ang pao money. The only difference is that our parents aren’t managing it for us anymore, so we end up spending the crap out of it. Our rational, adult minds tell ourselves that we should be saving and investing more, but our bratty kid selves simply don’t have that kind of self-control.

So here’s the problem: We want to save more, invest consistently, and pay all our bills on time, but we simply don’t have the discipline to do it. What should we do?

The answer: automate all of ’em. By automating, we can guarantee our success by forcing ourselves to comply with things that we know are right. For example, if I arrange to have $500 automatically transferred to a separate savings account every month, I essentially guarantee myself $500 of savings per month. Bam.

It sounds counterintuitive, but it’s often easier to succeed if you simply remove control from yourself.

It sets the stage for further automation

Automation is awesome for small tweaks like saving money or paying off your bills, but it’s got the potential to develop into a lot more. If you’re aiming to reach new levels of productivity, complete your own personal projects, or run your own business, you simply can’t run away from automation.

The best people, teams, and organizations have embraced automation for the same reasons we discussed: It frees up time and resources, and lets you focus on the important stuff and get the job done.

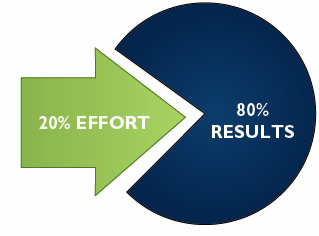

Tim Ferriss famously writes about how to automate your life in his book The 4-Hour Work Week. The book, in a nutshell, is how to apply the 80/20 rule – what are the 20% of activities you can focus on that will give you disproportionate results? As for the other 80% of not-so-crucial activities, how can you automate them?

An automated life isn’t just a nice thing to have; it’s critical for success. If you haven’t started automating bits of your life yet, then personal finance is an obvious place to start. Things like paying your bills or tracking your spending fall into the 80% category: they’re mundane, take up valuable time, but are still necessary. Why not automate them?

Once you get used to the idea of automating something as simple as your finances, it becomes a lot easier to apply those same principles to the bigger, more important, areas of your life and career.

I have just finished watching the video and I think it’s awesome. I shall try it.